Chapter 3 Supply And Demand Answers

Chapter 3 Supply And Demand Answers - Sum of all individual demands in a market. Five principal factors that shift the demand curve for a good service. Did the economic event affect supply or demand? 3.2 shifts in demand and supply for goods and services; Changes in the prices of related goods or services. Supply increases and demand is constant. Demand rises by the same amount that supply falls. Label the initial equilibrium price and quantity. From openstax principles of microeconomics (chapter 3) economists use the term demand to refer to the amount of some good or service consumers are willing and able to purchase at each price. C) demand for a good decreases and the supply of it increases.

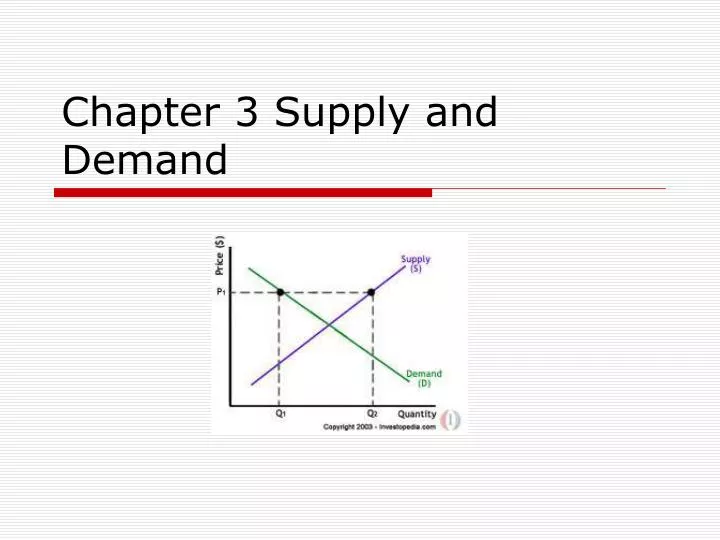

Web using the figures above, answer the following questions: 3.3 changes in equilibrium price and quantity: 1) a decrease in the price of a substitute leads to decrease in the qtd demanded for another good (pepsi price decreases, increase in demand. Is an institution which brings together buyers. Web 1) price of substitutes ( apple or pc) 2) price of compliments ( hamburger and hamburger bun) 3) income. Web introduction to demand and supply; C) demand for a good decreases and the supply of it increases. Demand increases and supply increases. 3.2 shifts in demand and supply for goods and services; Schedule showing a specific quantity of goods that suppliers are willing to provide at different prices.

Entails the exchange of goods, but not services. 1) a decrease in the price of a substitute leads to decrease in the qtd demanded for another good (pepsi price decreases, increase in demand. Web however, we cannot rule a shift in the supply curve as well. 3.3 changes in equilibrium price and quantity: Web substitutes goods that can serve as replacements for one another, when the price of one increases, demand for the other goes up market demand the total of all individual demands in a given market at a particular time price elasticity of demand. $\square$ show a decrease in quantity demanded. Supply falls and demand is constant. Web video answers for all textbook questions of chapter 3, supply and demand: Market situation where quantity of good supplied is fixed regardless of price. Demand rises by the same amount that supply falls.

CHapter 3 Answers Supply And Demand Demand

$\square$ show an increase in demand and label it d1. Five principal factors that shift the demand curve for a good service. Supply decreases and demand is constant. Demand falls and supply is constant. $\square$ show an increase in quantity demanded.

PPT Chapter 3 Demand and Supply PowerPoint Presentation, free

Demand increases and supply is constant. Market situation where quantity of good supplied is fixed regardless of price. Web 1) price of substitutes ( apple or pc) 2) price of compliments ( hamburger and hamburger bun) 3) income. 3.2 shifts in demand and supply for goods and services; Supply increases and demand decreases.

PPT Chapter 3 Demand & Supply PowerPoint Presentation, free download

Demand increases and supply increases. 123) the equilibrium quantity will decrease and the price might rise, fall, or stay the same when the a) demand. Demand rises more than supply. Draw the graph with the initial supply and demand curves. Supply increases and demand is constant.

Chapter 3 Supply and Demand

Web video answers for all textbook questions of chapter 3, supply and demand: 3.2 shifts in demand and supply for goods and services; 3.3 changes in equilibrium price and quantity: Web introduction to demand and supply; Web b) demand and the supply of a good both decrease.

Ppt Chapter 3 Demand Supply And Market Equilibrium Economics

Supply decreases and demand is constant. Web this chapter introduces the economic model of demand and supply—one of the most powerful models in all of economics. Is an institution which brings together buyers. 3.4 price ceilings and price floors; Web video answers for all textbook questions of chapter 3, supply and demand, coremacroeconomics by numerade

Shifting Supply And Demand Worksheet Answers Free Worksheet

Explain the impact of a change in demand or supply. 3.3 changes in equilibrium price and quantity: Is an institution which brings together buyers. 3.2 shifts in demand and supply for goods and services; Web 3 supply and demand 3.1 demand.

Chapter 3 Supply and Demand

Web 3 supply and demand 3.1 demand. Web video answers for all textbook questions of chapter 3, supply and demand: Web substitutes goods that can serve as replacements for one another, when the price of one increases, demand for the other goes up market demand the total of all individual demands in a given market at a particular time price.

Supply and Demand

Web substitutes goods that can serve as replacements for one another, when the price of one increases, demand for the other goes up market demand the total of all individual demands in a given market at a particular time price elasticity of demand. Market situation where quantity of good supplied is fixed regardless of price. 3.4 price ceilings and price.

PPT Chapter 3 Supply and Demand PowerPoint Presentation, free

Demand increases and supply is constant. Web a change in the quantity demanded of a good arising from a change in the good's price. The discussion here begins by examining how demand and supply determine the price and the quantity sold in markets for goods and services, and how changes in demand and supply. Understand the concepts of surpluses and.

Worksheet Chapter 3 Supply And Demand Answers Chapter Worksheet

Five principal factors that shift the demand curve for a good service. An increase in the price of jet fuel. Supply decreases and demand is constant. Draw the graph with the initial supply and demand curves. Supply rises and demand is constant.

Price Of Substitutes & Compliments.

Supply falls and demand is constant. 3.3 changes in equilibrium price and quantity: $\square$ show an increase in quantity demanded. $\square$ show a decrease in quantity demanded.

Web Use Supply And Demand Diagrams To Verify Your Answers.

Web 1) price of substitutes ( apple or pc) 2) price of compliments ( hamburger and hamburger bun) 3) income. Web b) demand and the supply of a good both decrease. From openstax principles of microeconomics (chapter 3) economists use the term demand to refer to the amount of some good or service consumers are willing and able to purchase at each price. Demand curve shifts rightward, supply curve shifts leftward, equilibrium price and quantity both rise.

Label The Initial Equilibrium Price And Quantity.

Demand increases and supply increases. Draw the graph with the initial supply and demand curves. Demand falls and supply is constant. The discussion here begins by examining how demand and supply determine the price and the quantity sold in markets for goods and services, and how changes in demand and supply.

Supply Decreases And Demand Is Constant.

Demand decreases and supply is constant. Supply rises and demand is constant. Supply increases and demand is constant. Web a change in the quantity demanded of a good arising from a change in the good's price.