Form 8594 Instructions

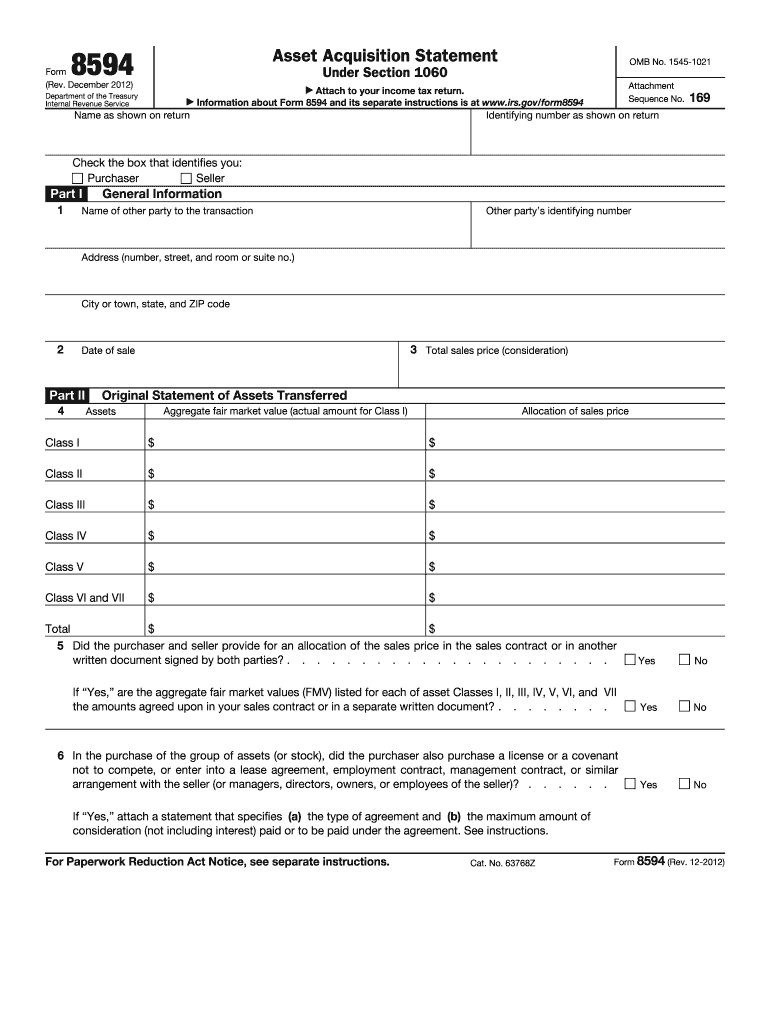

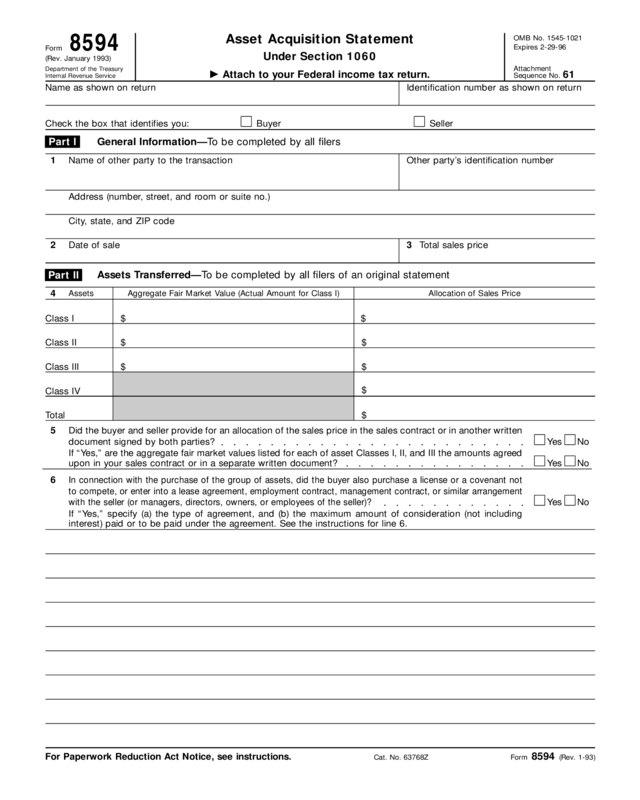

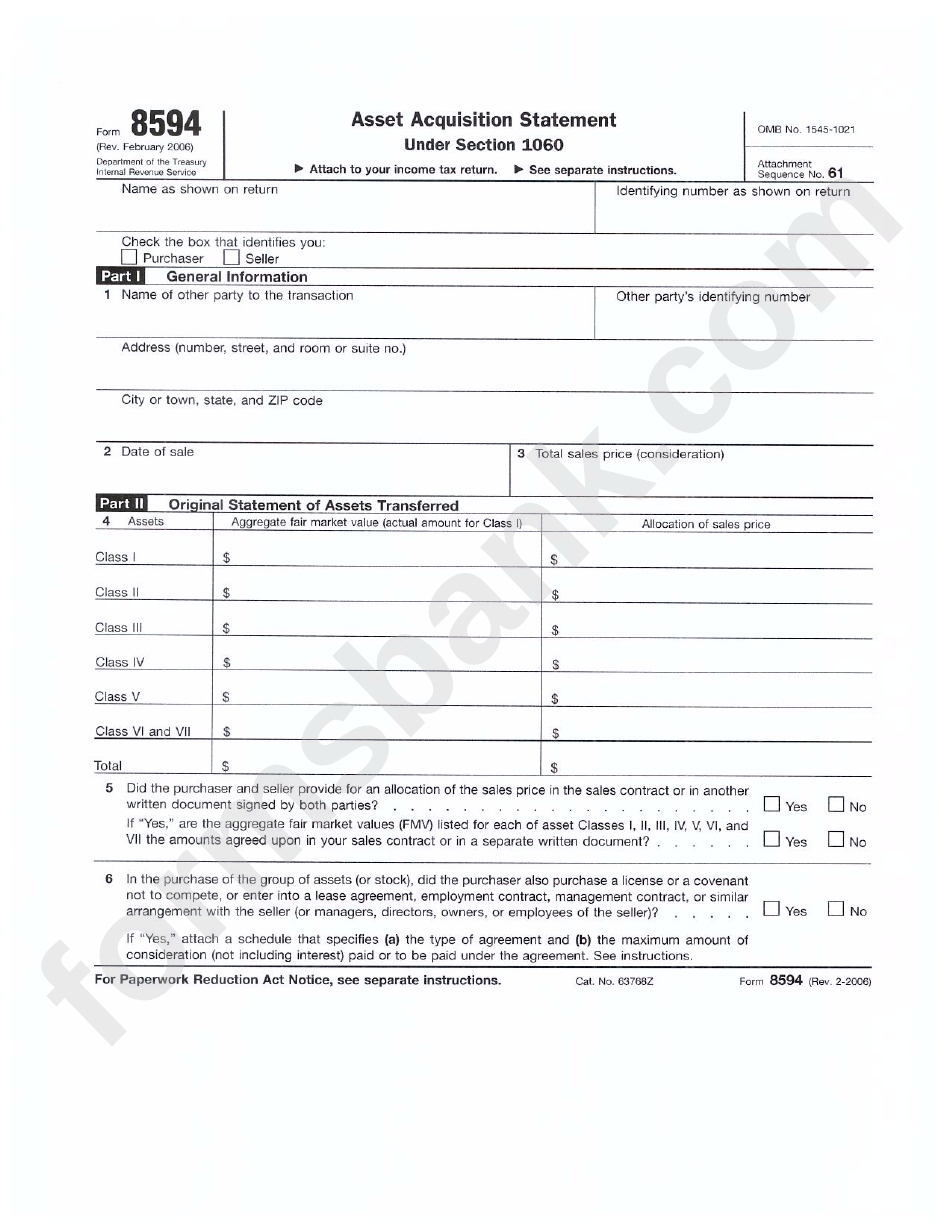

Form 8594 Instructions - For instructions and the latest information. The form must be filed when a group of assets were transferred (in a trade or business), and if the buyer’s basis in such assets is determined by the amount paid for the assets. If the amount allocated to any asset is increased or decreased after the year in which the sale occurs, the seller and/or purchaser (whoever is affected) must complete parts i and iii of form 8594 and attach the form to the income tax return for November 2021) department of the treasury internal revenue service. For asset acquisitions occurring after march 15, 2001, make the allocation among the following assets in proportion to (but not more than) their fair market value on the purchase date in the following order: Web instructions for form 8594. Web we last updated the asset acquisition statement under section 1060 in february 2023, so this is the latest version of form 8594, fully updated for tax year 2022. The buyers and sellers of a group of assets that make up a business use form 8594 when goodwill or going concern value attaches. The following income tax return for the year in which the definitions are the classifications for Web information about form 8594, asset acquisition statement under section 1060, including recent updates, related forms and instructions on how to file.

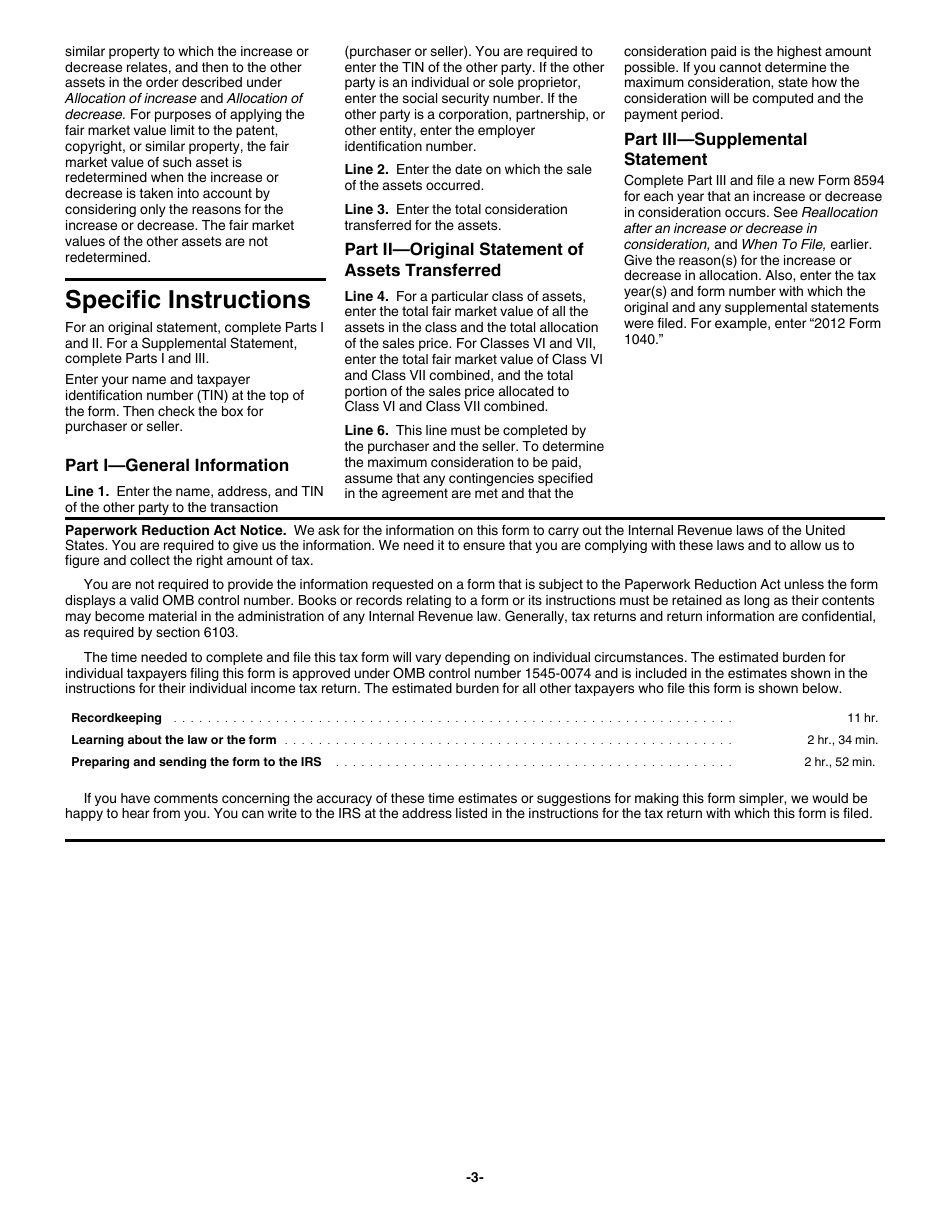

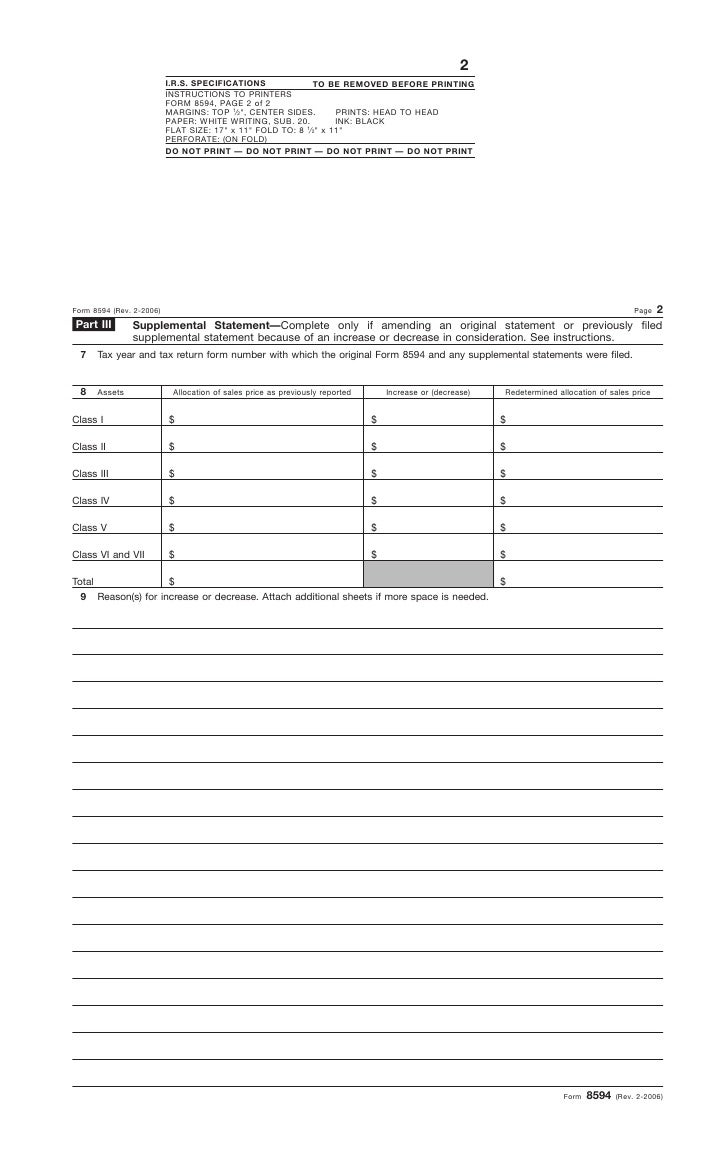

If the amount allocated to any asset is increased or decreased after the year in which the sale occurs, the seller and/or purchaser (whoever is affected) must complete parts i and iii of form 8594 and attach the form to the income tax return for The form must be filed when a group of assets were transferred (in a trade or business), and if the buyer’s basis in such assets is determined by the amount paid for the assets. Web generally, attach form 8594 to your income tax return for the year in which the sale date occurred. For asset acquisitions occurring after march 15, 2001, make the allocation among the following assets in proportion to (but not more than) their fair market value on the purchase date in the following order: The buyers and sellers of a group of assets that make up a business use form 8594 when goodwill or going concern value attaches. Failure to file the required documents may result in penalties. Web information about form 8594, asset acquisition statement under section 1060, including recent updates, related forms and instructions on how to file. Cash and general deposit accounts (including savings and checking accounts) other than certificates of deposit held in bank,s, savings and loan associations, and other depository institutions. Both the seller and purchaser of a group of assets that makes up a trade or business must use form 8594 to report such a sale if goodwill or going concern value attaches, or could attach, to such assets and if the purchaser's basis in the assets is determined only by the amount paid for the assets. The following income tax return for the year in which the definitions are the classifications for

You can print other federal tax forms here. Web irs form 8594 instructions lists the following seven classes of assets: For instructions and the latest information. For asset acquisitions occurring after march 15, 2001, make the allocation among the following assets in proportion to (but not more than) their fair market value on the purchase date in the following order: Web form 8594 instructions list seven classes of assets. Web instructions for form 8594. Web information about form 8594, asset acquisition statement under section 1060, including recent updates, related forms and instructions on how to file. The irs instructs that both the buyer and seller must file the form and attach their income tax returns. If the amount allocated to any asset is increased or decreased after the year in which the sale occurs, the seller and/or purchaser (whoever is affected) must complete parts i and iii of form 8594 and attach the form to the income tax return for The buyer or seller must also update the amount allocated to the asset on his or her income tax return.

Form 8594 Instructions Fill Out and Sign Printable PDF Template signNow

November 2021) department of the treasury internal revenue service. You can print other federal tax forms here. Cash and general deposit accounts (including savings and checking accounts) other than certificates of deposit held in bank,s, savings and loan associations, and other depository institutions. Purpose of form generally, attach form 8594 to your classes of assets. Both the seller and purchaser.

Download Instructions for IRS Form 8594 Asset Acquisition Statement

Both the seller and purchaser of a group of assets that makes up a trade or business must use form 8594 to report such a sale if goodwill or going concern value attaches, or could attach, to such assets and if the purchaser's basis in the assets is determined only by the amount paid for the assets. Web instructions for.

Fillable Form Dss8594 Notice Of Expiration North Carolina

Web generally, attach form 8594 to your income tax return for the year in which the sale date occurred. November 2021) department of the treasury internal revenue service. Web the irs form 8594 must be completed and attached to an income tax return by the buyer or seller. The following income tax return for the year in which the definitions.

Solved ACCT 538 Form 8594 assignment Readorly Insert Draw

Web information about form 8594, asset acquisition statement under section 1060, including recent updates, related forms and instructions on how to file. Purpose of form generally, attach form 8594 to your classes of assets. Cash and general deposit accounts (including savings and checking accounts) other than certificates of deposit held in bank,s, savings and loan associations, and other depository institutions..

Form 8594 Edit, Fill, Sign Online Handypdf

The buyers and sellers of a group of assets that make up a business use form 8594 when goodwill or going concern value attaches. Web form 8594 instructions list seven classes of assets. For asset acquisitions occurring after march 15, 2001, make the allocation among the following assets in proportion to (but not more than) their fair market value on.

Form 8594 Asset Acquisition Statement Under Section 1060 Internal

For asset acquisitions occurring after march 15, 2001, make the allocation among the following assets in proportion to (but not more than) their fair market value on the purchase date in the following order: Failure to file the required documents may result in penalties. Attach to your income tax return. The following income tax return for the year in which.

Instructions for Form 8594

Than any nonrecourse debt to which the when to file property is subject. The following income tax return for the year in which the definitions are the classifications for The irs instructs that both the buyer and seller must file the form and attach their income tax returns. Both the seller and purchaser of a group of assets that makes.

IRS Form 8938 How to Fill it with the Best Form Filler

November 2021) department of the treasury internal revenue service. Web irs form 8594 instructions lists the following seven classes of assets: Cash and general deposit accounts (including savings and checking accounts) other than certificates of deposit held in bank,s, savings and loan associations, and other depository institutions. The buyer or seller must also update the amount allocated to the asset.

How Many of the 5,211 Former U.S. Citizens (who Renounced in 2014 and

The buyer or seller must also update the amount allocated to the asset on his or her income tax return. Cash and general deposit accounts (including savings and checking accounts) other than certificates of deposit held in bank,s, savings and loan associations, and other depository institutions. Web generally, attach form 8594 to your income tax return for the year in.

Form 8594Asset Acquisition Statement

For asset acquisitions occurring after march 15, 2001, make the allocation among the following assets in proportion to (but not more than) their fair market value on the purchase date in the following order: Failure to file the required documents may result in penalties. The buyers and sellers of a group of assets that make up a business use form.

The Buyer Or Seller Must Also Update The Amount Allocated To The Asset On His Or Her Income Tax Return.

Both the seller and purchaser of a group of assets that makes up a trade or business must use form 8594 to report such a sale if goodwill or going concern value attaches, or could attach, to such assets and if the purchaser's basis in the assets is determined only by the amount paid for the assets. The buyers and sellers of a group of assets that make up a business use form 8594 when goodwill or going concern value attaches. Attach to your income tax return. Failure to file the required documents may result in penalties.

For Asset Acquisitions Occurring After March 15, 2001, Make The Allocation Among The Following Assets In Proportion To (But Not More Than) Their Fair Market Value On The Purchase Date In The Following Order:

Web the irs form 8594 must be completed and attached to an income tax return by the buyer or seller. You can print other federal tax forms here. Web we last updated the asset acquisition statement under section 1060 in february 2023, so this is the latest version of form 8594, fully updated for tax year 2022. If the amount allocated to any asset is increased or decreased after the year in which the sale occurs, the seller and/or purchaser (whoever is affected) must complete parts i and iii of form 8594 and attach the form to the income tax return for

For Instructions And The Latest Information.

The irs instructs that both the buyer and seller must file the form and attach their income tax returns. Web form 8594 instructions list seven classes of assets. November 2021) department of the treasury internal revenue service. Web generally, attach form 8594 to your income tax return for the year in which the sale date occurred.

Web Instructions For Form 8594.

Purpose of form generally, attach form 8594 to your classes of assets. The form must be filed when a group of assets were transferred (in a trade or business), and if the buyer’s basis in such assets is determined by the amount paid for the assets. The following income tax return for the year in which the definitions are the classifications for Cash and general deposit accounts (including savings and checking accounts) other than certificates of deposit held in bank,s, savings and loan associations, and other depository institutions.